Category: Accountancy

-

Debits vs Credits in Modern Accounting Software: New Rules Explained

Core Principles of Debits and Credits Every accounting transaction affects at least two accounts through debits and credits. Specific rules based on the accounting equation and account type determine whether debits or credits increase or decrease account balances. Understanding the Accounting Equation The accounting equation forms the foundation of all debit and credit entries: Assets…

-

Real-World Examples of Debits and Credits: Everyday Accounting Scenarios

Understanding the Core Principles of Debits and Credits Accountants use debits and credits together in every transaction to keep financial records accurate. Each debit entry always matches a credit entry of equal value. What Are Debits and Credits? Debits and credits are the basic terms for recording financial transactions. A debit records an amount on…

-

Debits and Credits for Small Business Owners: Essential Concepts and Best Practices

Understanding Debits and Credits in Accounting Debits and credits are the two sides of every financial transaction a business records. Each debit entry pairs with a matching credit entry of the same amount. Understanding how debits and credits affect different accounts helps business owners track money flowing in and out of their company. Defining Debits…

-

The History of Debits and Credits: Tracing the Foundations of Modern Accounting

Origins of Bookkeeping and Early Business Transactions Bookkeepers in ancient civilizations began tracking goods, taxes, and trade over 7,000 years ago. These early systems became the basis for modern accounting by teaching people how to document business transactions and keep financial records. Ancient Mesopotamian Record-Keeping People in ancient Mesopotamia started keeping accounting records more than…

-

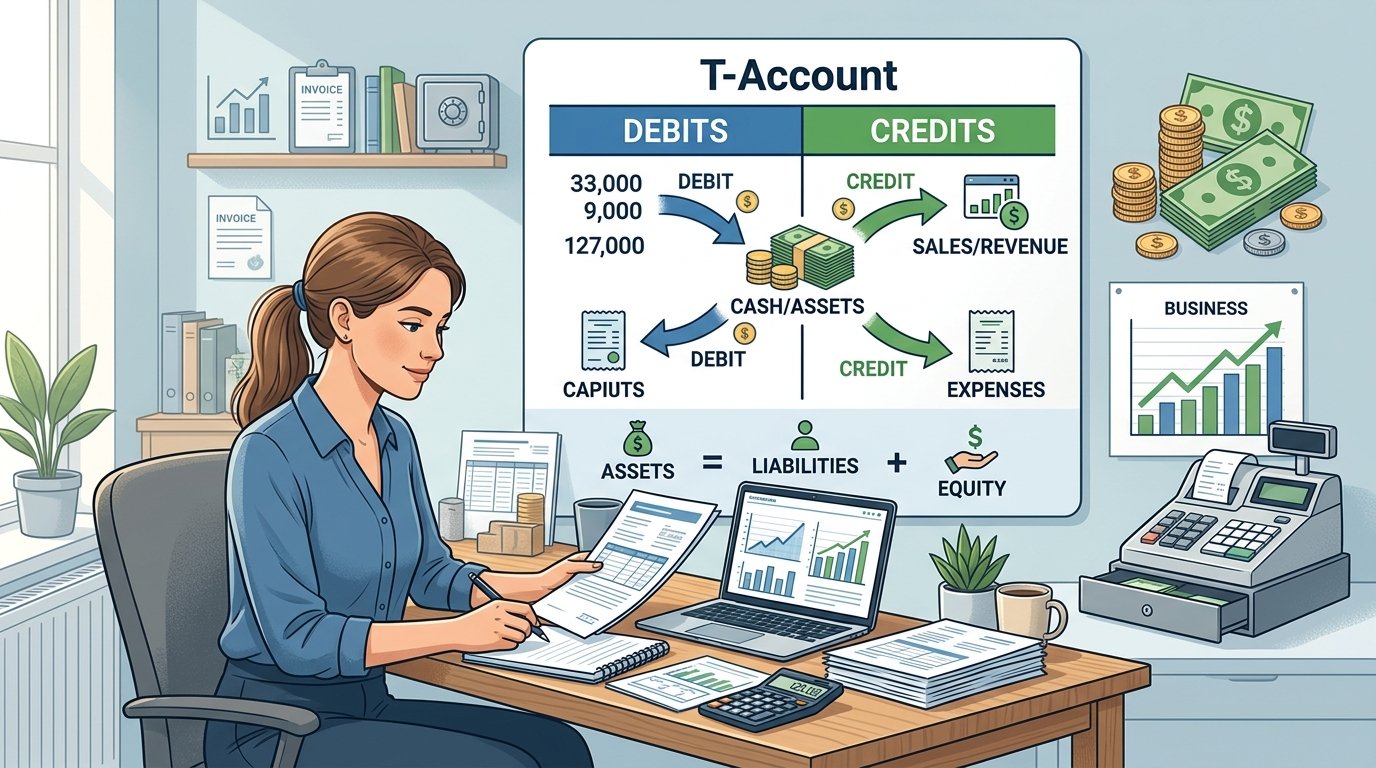

Understanding T-Accounts: Debits, Credits, and Visual Accounting

Core Structure and Function of T-Accounts A T-account uses a simple “T” shape to organize financial information. The account name sits at the top, and two sides separate debits from credits. This format helps people track how money moves in and out of each ledger account. Visual Format and Components A T-account looks like the…

-

From Receipts to Reports: Step-by-Step Guide to Accurate Financial Records

Understanding Source Documents and Transaction Recording Every financial transaction begins with a source document and moves through a systematic recording process. Bookkeepers identify transactions, make accurate journal entries, and apply accounting methods consistently. The Role of Receipts, Invoices, and Source Documents Source documents provide physical or electronic evidence for financial transactions. These documents create a…

-

Financial Statements Demystified: Unlocking Bookkeeping Insights

Understanding the Core Financial Statements Financial statements turn bookkeeping data into three primary reports that show a company’s financial position and performance. These documents—the balance sheet, income statement, and cash flow statement—work together with supporting notes to give a full view of business operations. Balance Sheet Fundamentals The balance sheet lists what a company owns…

-

Scaling Your Skills: Transitioning from Bookkeeper to Accountant for Career Growth

Key Role Differences and Skill Expansion When you move from bookkeeper to accountant, you need to understand how your daily work changes. You also need to develop analytical capabilities that go beyond recording transactions. This shift brings broader responsibilities, strategic thinking, and enhanced technical expertise. Daily Responsibilities and Scope Change Bookkeepers record financial transactions as…

-

From Data Entry to Data Strategy: How AI Transforms Accountancy

Automating the Foundations: AI in Data Entry and Transaction Processing Artificial intelligence now completes core bookkeeping tasks quickly and consistently. It captures data, matches transactions, and flags issues in real time. This shift lets accountants focus on review and strategy instead of manual entry. AI-Powered Data Capture and ICR AI-powered data capture replaces manual typing…

-

From CPA Candidate to Confident Professional: Your Step-by-Step U.S. Accounting Career Guide

Essential Steps for Becoming an Accountant The accounting profession offers many career paths, such as public accounting and specialized roles in tax or forensics. You can succeed by learning about the field, setting clear goals, and choosing the accounting role that fits your skills and interests. Understanding the Accounting Profession Accountants record, analyze, and report…

-

Choosing Your Path in Accounting: Guide to Public, Private, Government, and Nonprofit Careers

Key Differences Among Public, Private, Government, and Nonprofit Accounting Each accounting career path serves different clients and follows unique reporting rules. Public and private accounting focus on business needs. Government and nonprofit accounting prioritize public service and donor accountability. Scope of Work and Services Public accounting firms serve multiple external clients at once. These firms…

-

How to Prepare for and Pass the CPA Exam: Proven First-Time Success Strategies

Understanding the CPA Exam Structure and Pathways The Uniform CPA Examination uses a Core + Discipline model. Candidates complete three mandatory Core sections and select one Discipline section that fits their career goals. Candidates must score at least 75 on each section to earn a CPA license. Overview of Uniform CPA Examination Format The Uniform…

-

Building Your First Client Base: Essential Steps for Accountants

Defining Your Ideal Client and Service Offering New independent accountants must define who they serve and what services they provide before they start marketing their practice. These choices affect pricing, marketing messages, and daily work satisfaction. Identifying Your Target Market A clear ideal client profile helps new accountants avoid wasting time on prospects who are…

-

Essential Tech Tools and Software Every New Accountant Should Master: The Modern Digital Toolkit

Core Accounting Software Platforms New accountants must learn the main accounting software platforms used in the profession. QuickBooks Online leads the market with comprehensive features. Xero excels in cloud-based solutions and multi-user access. Sage provides robust desktop and cloud options for complex needs. FreshBooks and Wave offer streamlined tools for specific business types. QuickBooks and…

-

Understanding U.S. Tax Law Basics: Essential Guide for Entry-Level Accountants

Key Foundations of U.S. Tax Law The U.S. tax system operates through multiple layers of government authority. Each level has specific powers to collect taxes. The Internal Revenue Service enforces federal tax laws through regulations and audits. Constitutional provisions and statutes create the legal framework. Federal, State, and Local Tax Structures The U.S. tax system…

-

Ethics and Compliance in U.S. Accounting: Essential Guidelines for New Professionals

Foundational Principles of Accounting Ethics Specific principles guide professional conduct and decision-making in accounting. These principles set clear expectations for independence, objectivity, and professional behavior. Accountants rely on these principles to address ethical responsibilities in practice. Core Ethical Principles and Values Five fundamental principles form the foundation of professional accounting ethics in the AICPA Code…

-

Networking for Accountants: Building Relationships for Career Success

Types of Professional Networks in Accounting Accountants use three main types of professional networks during their careers. Operational networking handles daily work needs, personal networking supports individual growth, and strategic networking positions professionals for future advancement. Operational Networking Explained Operational networking involves the connections accountants need to complete their current job responsibilities. This network includes…

-

Setting Up Your Own Accounting Firm: Essential Legal, Financial, and Operational Steps

Choosing Your Business Structure Your business structure affects your tax obligations, personal liability, and operational requirements. Accounting professionals usually choose between sole proprietorships, partnerships, and corporations based on growth plans and risk tolerance. Sole Proprietorships: Pros and Cons A sole proprietorship is the simplest structure for an accounting firm owner working alone. You only need…

-

Career Growth in Accounting: Certifications, Specializations, and Planning

Essential Certifications for Advancing Your Accounting Career Professional certifications prove expertise and help accountants qualify for higher-level positions. The CPA is the most recognized credential in public accounting. Certifications like the CMA and CIA help professionals in corporate and internal audit roles. Specialized credentials address areas such as fraud examination and government finance. CPA: The…

-

Generative AI for Tax Professionals: Streamlining Research & Client Communication

Generative AI in Tax Practice: Core Concepts and Benefits Generative AI is changing how tax professionals research rules, draft reports, and communicate with clients. It builds on advances in artificial intelligence and machine learning to produce usable text, summaries, and analysis from large data sets. What Is Generative AI and How Does It Work? Generative…