Author: Dennis Smith

-

What Are the Most Innovative Accounting Automation Tools Available Today: Unveiling the Future of Finances

Overview of Accounting Automation Accounting automation refers to the use of technology to complete accounting tasks with minimal human intervention. This typically involves software systems that can handle repetitive and time-consuming tasks, reducing errors and freeing accountants to focus on more strategic functions. Key Functions: Advantages include: Types of Automation Tools: Popular Tools: Tool Name…

-

How Does Accounting Automation Affect Financial Data Security? Unpacking the Implications

Overview of Accounting Automation Accounting automation refers to the use of software and digital processes to handle accounting tasks traditionally performed manually. Automation software can carry out repetitive functions such as data entry, reconciliations, and report generation with greater efficiency and reduced human intervention. The rise of cloud-based platforms has also enhanced accessibility and collaboration,…

-

What Impact Does Accounting Automation Have on Financial Accuracy and Compliance: Enhancing Precision and Adherence

Overview of Accounting Automation Accounting automation refers to the use of various software and technological tools to conduct accounting tasks with minimal human intervention. This technology simplifies, streamlines, and enhances the efficiency of the financial recording and reporting processes. Automation tools range from basic applications for bookkeeping to advanced systems that integrate business intelligence and…

-

How Can Small Businesses Get Started with Accounting Automation: A Step-by-Step Guide

Understanding Accounting Automation Accounting automation refers to the use of software to manage financial transactions and bookkeeping tasks, streamlining processes that were traditionally manual. Defining Accounting Automation Accounting automation involves the replacement of manual data entry and financial management processes with software capable of handling these tasks with minimal human intervention. Key components typically include:…

-

What Are the Best Practices for Transitioning to Automated Accounting Systems: A Step-by-Step Guide for Businesses

Understanding Automated Accounting Systems Automated accounting systems are software solutions designed to manage a business’s financial transactions and records with minimal human intervention. They integrate various accounting tasks, including bookkeeping, invoicing, payroll, and reporting, into one streamlined process. The key features of these systems often include: Businesses considering the transition to an automated system should…

-

Debits and Credits for Small Business Owners: Essential Concepts and Best Practices

Understanding Debits and Credits in Accounting Debits and credits are the two sides of every financial transaction a business records. Each debit entry pairs with a matching credit entry of the same amount. Understanding how debits and credits affect different accounts helps business owners track money flowing in and out of their company. Defining Debits…

-

Which Accounting Tasks Can Be Automated and Which Shouldn’t: Striking the Right Balance

Fundamentals of Accounting Automation Accounting automation refers to the use of software tools to perform accounting tasks with minimal human intervention. These tools rely on algorithms and predetermined rules to process financial transactions, manage data, and generate reports. Automation in accounting can significantly increase efficiency, reduce errors, and streamline workflows. Key Components of Accounting Automation:…

-

What Are the Key Benefits and Risks of Accounting Automation: Advantages and Pitfalls Analysis

Overview of Accounting Automation Accounting automation refers to the use of digital tools and software to manage and record financial transactions and processes with minimal human intervention. It involves applying technology to traditional accounting tasks such as data entry, invoice processing, and reconciliation. Key Components: Capabilities: By automating these processes, businesses can streamline financial operations,…

-

How Does Automated Accounting Change the Role of Traditional Accountants: Impact and Adaptation

Overview of Automated Accounting Automated accounting encompasses the use of software to handle routine financial transactions and processes traditionally performed by accountants. This technology streamlines data entry, reconciliations, and report generation, reducing the need for manual intervention. Key Components: Impact on Accounting: Adoption Rates:A survey by Sage reported a significant increase in this technology’s adoption,…

-

The History of Debits and Credits: Tracing the Foundations of Modern Accounting

Origins of Bookkeeping and Early Business Transactions Bookkeepers in ancient civilizations began tracking goods, taxes, and trade over 7,000 years ago. These early systems became the basis for modern accounting by teaching people how to document business transactions and keep financial records. Ancient Mesopotamian Record-Keeping People in ancient Mesopotamia started keeping accounting records more than…

-

How an Inventory Write-Down Affects the Three Statements

Inventory write-downs are a common occurrence in the business world. They happen when a company’s inventory is worth less than its recorded value on the balance sheet. This can happen for a variety of reasons, such as spoilage, obsolescence, or damage. When this occurs, the company must adjust its financial statements to reflect the new,…

-

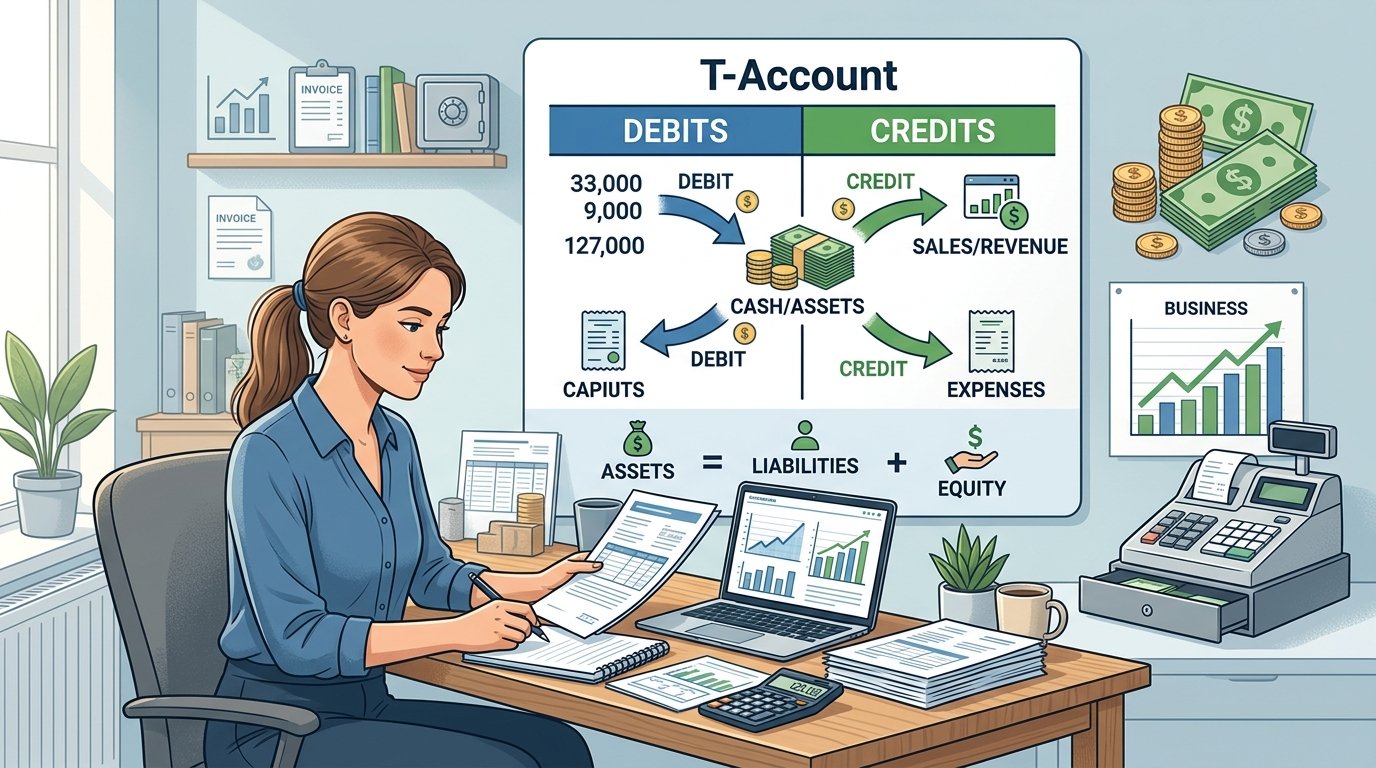

Understanding T-Accounts: Debits, Credits, and Visual Accounting

Core Structure and Function of T-Accounts A T-account uses a simple “T” shape to organize financial information. The account name sits at the top, and two sides separate debits from credits. This format helps people track how money moves in and out of each ledger account. Visual Format and Components A T-account looks like the…

-

From Receipts to Reports: Step-by-Step Guide to Accurate Financial Records

Understanding Source Documents and Transaction Recording Every financial transaction begins with a source document and moves through a systematic recording process. Bookkeepers identify transactions, make accurate journal entries, and apply accounting methods consistently. The Role of Receipts, Invoices, and Source Documents Source documents provide physical or electronic evidence for financial transactions. These documents create a…

-

Accounting Normalization: A Clear Explanation

Accounting normalization is a process that helps companies to adjust their financial statements to reflect the true economic reality of their business operations. The purpose of accounting normalization is to remove any distortions or anomalies in the financial statements caused by non-recurring events or accounting policies that do not reflect the true economic impact of…

-

How to Track Business Expenses Effectively in Bookkeeping: Essential Strategies

Tracking business expenses is a fundamental aspect of running a company, providing a clear picture of the financial health of an organization. By effectively recording all financial transactions, businesses can ensure accurate financial reporting and analysis, which in turn supports smarter decision-making. The process involves a detailed recording of purchases, sales, receipts, and payments, outlining…

-

Is It Necessary to Have a Business Plan?

Many entrepreneurs and business owners often wonder whether or not having a business plan is necessary. Some argue that it’s a waste of time and resources, while others believe it’s a crucial step towards success. The truth is, having a business plan can make a significant difference in the success of a business. Understanding the…

-

What is the Importance of a Budget in Bookkeeping? Unveiling its Role in Financial Management

A budget plays a crucial role in the realm of bookkeeping, providing a structured approach to financial management. By establishing a budget, businesses can set clear financial targets, allocate resources efficiently, and monitor the organization’s cash flow with precision. The budget serves as a roadmap, guiding both short-term expenditures and long-term investments, ensuring that business…

-

Small Business Bookkeeping: Practical Skills for Success

Foundations of Small Business Bookkeeping Small business bookkeeping provides a system for tracking money, organizing transactions, and keeping accurate financial records. These practices support daily operations and help businesses prepare for more advanced accounting. Understanding the Role of Bookkeeping Bookkeepers record every financial transaction a business makes each day. They track sales, purchases, payments, and…

-

Functions of Accounting: A Clear Explanation

Accounting is a crucial aspect of any business, regardless of its size or industry. It involves the process of recording, classifying, and summarizing financial transactions to provide relevant information for decision-making purposes. Accounting provides a comprehensive overview of a company’s financial health, which is essential for its survival and growth. The primary function of accounting…

-

How to Calculate Break-Even Point in Bookkeeping: A Step-by-Step Guide

Calculating the break-even point is a fundamental aspect of bookkeeping that enables business owners to understand when their company will be able to cover all its costs with the revenue generated from sales. It represents a critical juncture in financial analysis where total costs equal total revenue, and profit generation begins beyond this point. Significance…