Category: Double-entry Bookkeeping

-

Debits vs Credits in Modern Accounting Software: New Rules Explained

Core Principles of Debits and Credits Every accounting transaction affects at least two accounts through debits and credits. Specific rules based on the accounting equation and account type determine whether debits or credits increase or decrease account balances. Understanding the Accounting Equation The accounting equation forms the foundation of all debit and credit entries: Assets…

-

Real-World Examples of Debits and Credits: Everyday Accounting Scenarios

Understanding the Core Principles of Debits and Credits Accountants use debits and credits together in every transaction to keep financial records accurate. Each debit entry always matches a credit entry of equal value. What Are Debits and Credits? Debits and credits are the basic terms for recording financial transactions. A debit records an amount on…

-

Debits and Credits for Small Business Owners: Essential Concepts and Best Practices

Understanding Debits and Credits in Accounting Debits and credits are the two sides of every financial transaction a business records. Each debit entry pairs with a matching credit entry of the same amount. Understanding how debits and credits affect different accounts helps business owners track money flowing in and out of their company. Defining Debits…

-

The History of Debits and Credits: Tracing the Foundations of Modern Accounting

Origins of Bookkeeping and Early Business Transactions Bookkeepers in ancient civilizations began tracking goods, taxes, and trade over 7,000 years ago. These early systems became the basis for modern accounting by teaching people how to document business transactions and keep financial records. Ancient Mesopotamian Record-Keeping People in ancient Mesopotamia started keeping accounting records more than…

-

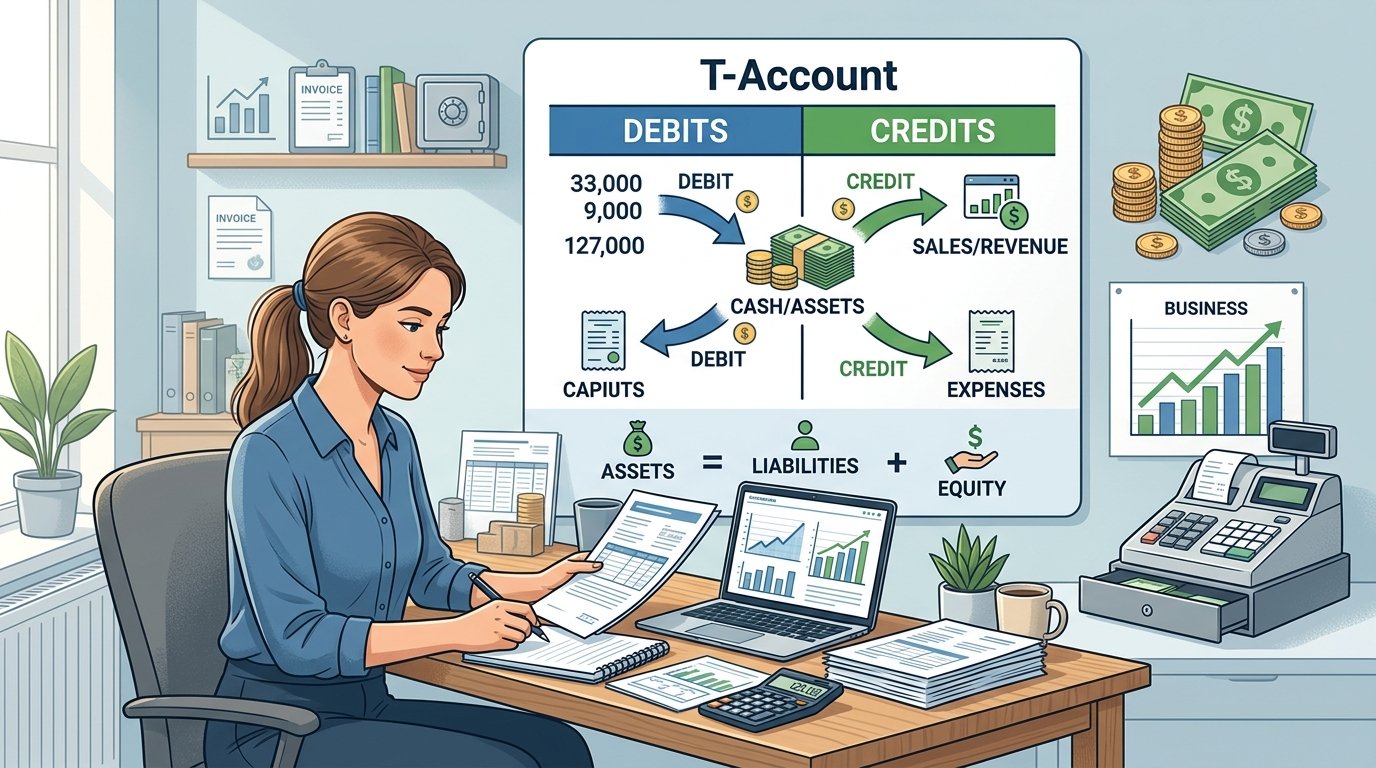

Understanding T-Accounts: Debits, Credits, and Visual Accounting

Core Structure and Function of T-Accounts A T-account uses a simple “T” shape to organize financial information. The account name sits at the top, and two sides separate debits from credits. This format helps people track how money moves in and out of each ledger account. Visual Format and Components A T-account looks like the…

-

The Complete Bookkeeping Roadmap: Essential Skills and Processes

Core Bookkeeping Principles Every business uses specific rules to keep financial data accurate and balanced. Double-entry bookkeeping requires each transaction to affect at least two accounts. Journals and ledgers organize this information from the initial recording to final account balances. Understanding Double-Entry Bookkeeping Double-entry bookkeeping forms the foundation of modern accounting. Each transaction must affect…

-

Starting Strong: Essential Training for Junior Accountants

Core Technical Skills for Junior Accountants Accurate financial records, organized systems, and reliable tools form the backbone of strong accounting work. Junior accountants develop technical skills to track transactions, prepare reports, and analyze financial data for daily business decisions. Mastering Double-Entry Bookkeeping Double-entry bookkeeping is the basis of modern accounting. Every transaction involves at least…

-

Mastering the Accounting Equation: Essential Tips and Tricks for Accurate Financial Analysis

Understanding the Accounting Equation The accounting equation forms the basis of double-entry bookkeeping. It shows how a company’s assets, liabilities, and equity connect and stay in balance. Understanding each part helps track financial health and report accurately. Definition and Components The accounting equation is: Assets = Liabilities + Equity This equation shows that a business…

-

Understanding Debits and Credits in Bookkeeping and Accounting: A Comprehensive Guide

The Fundamentals of Debits and Credits Debits and credits are essential to bookkeeping and accounting. They track changes in financial accounts and keep the books balanced. Each transaction affects at least two accounts. One side receives a debit, and the other receives a credit to show increases or decreases. The Role of Debits and Credits…

-

Debits vs Credits: The Student’s Ultimate Guide to Mastering Accounting Basics

Understanding Debits and Credits Debits and credits form the base of accounting. Accountants use them to record every financial transaction and keep the books balanced. Each term has a specific meaning in tracking money moving in and out of accounts. Definition of Debits A debit is an entry on the left side of an account.…

-

Double-entry Accounting Explained In Simple Terms

Double-entry accounting is really very simple provided you follow these rules. For a Transaction to be true to the double-entry principle, two further rules must be obeyed: Furthermore, each entry must consist of a minimum of four pieces of information as follows: 1. Date (the date on which the transaction occurred)2. Reference (so it can…

-

Learn Double-Entry Bookkeeping

Here’s a great resource from Loris Tissino. He has developed a site to step you through double-entry including transactions and posting. I think you will find this another very useful tool. Loris has written a piece for Accounting for Everyone describing it. Here we go: If you are a student and want to practice bookkeeping…