Understanding Debits and Credits in Accounting

Debits and credits are the two sides of every financial transaction a business records. Each debit entry pairs with a matching credit entry of the same amount.

Understanding how debits and credits affect different accounts helps business owners track money flowing in and out of their company.

Defining Debits and Credits

A debit is an accounting entry that goes on the left side of a ledger. Debits increase assets and expenses and decrease liabilities, equity, and revenue.

When a business buys equipment or pays rent, it records debits for those transactions. A credit is an entry on the right side of a ledger.

Credits increase liabilities, equity, and revenue and decrease assets and expenses. Taking out a loan or making a sale both use credits.

The terms “debit” and “credit” don’t mean “good” or “bad.” They simply show which side of the accounting equation changes.

Every transaction needs both a debit and a credit to keep the books balanced. Business owners often abbreviate these terms as “DR” for debit and “CR” for credit in their records.

The Role of Debits and Credits in Business Finances

Debits and credits form the foundation of double-entry bookkeeping. This system requires every transaction to affect at least two accounts equally.

The accounting equation drives this system: Assets = Liabilities + Equity. When a business records transactions, debits and credits keep this equation balanced.

For example, when a business takes out a $5,000 loan to buy equipment, it debits the equipment account for $5,000 and credits the loan payable account for $5,000.

Both sides of the equation stay equal. Business owners can trust their profit and loss statements and balance sheets when they record debits and credits correctly.

Debits vs. Credits: Key Differences and Myths

The main difference between debits and credits is which accounts they increase. Each account type has a “normal balance” that shows whether it naturally increases with debits or credits.

| Account Type | Increased By | Decreased By |

|---|---|---|

| Assets | Debit | Credit |

| Expenses | Debit | Credit |

| Liabilities | Credit | Debit |

| Equity | Credit | Debit |

| Revenue | Credit | Debit |

A common myth is that debits always mean money coming in and credits mean money going out. This isn’t true.

When a business pays cash for supplies, it debits the supplies account (increasing assets) and credits the cash account (decreasing assets). Both entries involve assets, but one increases while the other decreases.

Another misconception is that credits are always good for a business. A credit to revenue is positive, but a credit to an expense account during a refund reverses a previous entry.

The impact depends entirely on which account receives the credit.

How Double-Entry Bookkeeping Works

Double-entry bookkeeping tracks every transaction in two places. Each transaction affects at least two accounts, with equal debits and credits that keep the books balanced.

The Double-Entry Accounting System

The double-entry accounting system records every transaction twice: once as a debit and once as a credit. This method keeps the accounting equation balanced after each entry.

When a business receives cash from a sale, the cash account increases and the sales revenue account also increases by the same amount. Every entry in this system has an equal and opposite entry.

If a business buys equipment for $5,000, the equipment account increases by $5,000 and the cash account decreases by $5,000. The total debits always equal the total credits.

This system helps catch errors. When debits and credits don’t match, it signals a mistake.

The Accounting Equation Explained

The accounting equation forms the foundation of double-entry bookkeeping: Assets = Liabilities + Equity. Assets are what the business owns, liabilities are what it owes, and equity represents the owner’s stake.

Every transaction keeps this equation in balance. When a business takes out a $10,000 loan, assets (cash) increase by $10,000 and liabilities (loan payable) increase by $10,000.

The equation also shows how profit affects the business. When a company earns revenue, equity increases. When it pays expenses, equity decreases.

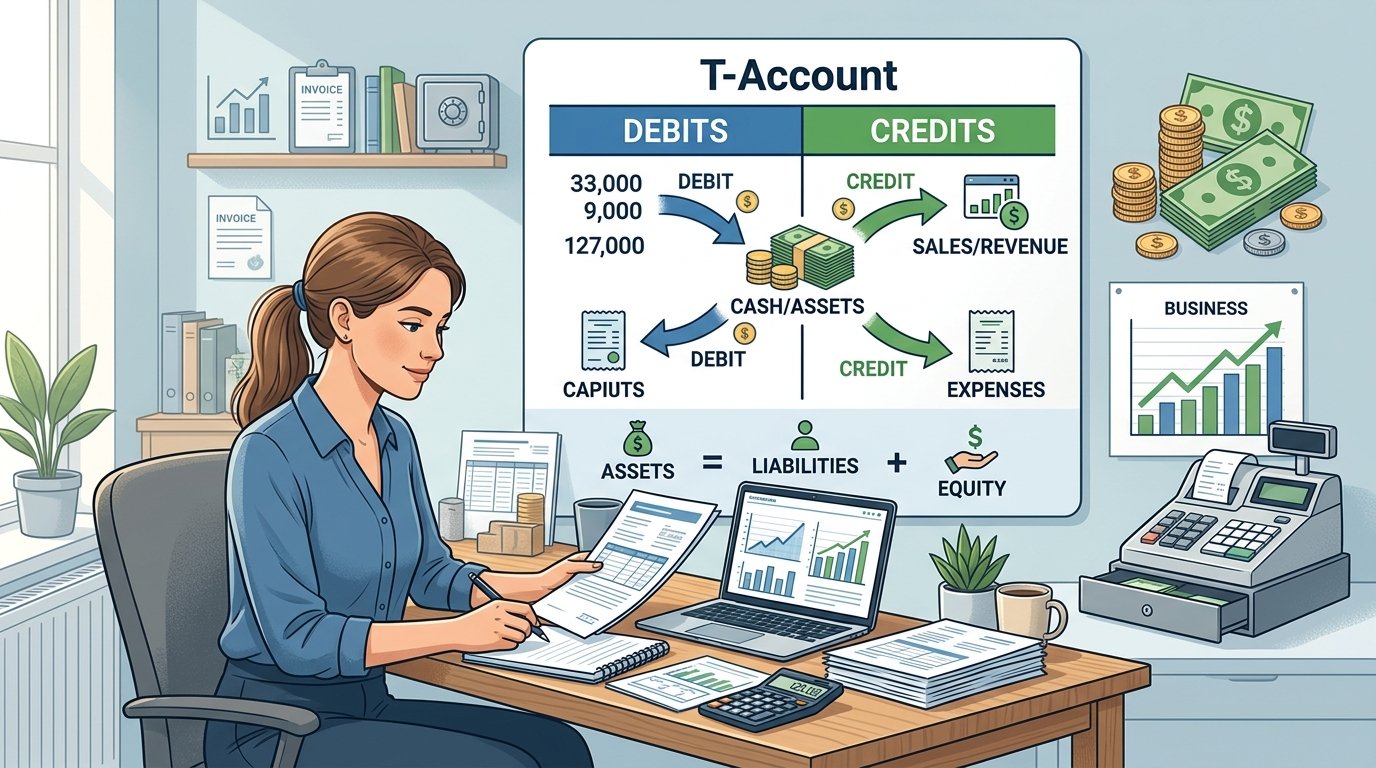

T-Accounts and Journal Entries Overview

A t-account is a visual tool that shows debits on the left side and credits on the right side. The account name sits at the top, with a “T” shape dividing the two sides.

Business owners use t-accounts to track how transactions affect individual accounts before entering them in the general ledger.

Journal entries record transactions in chronological order. Each journal entry includes the date, the accounts affected, the debit and credit amounts, and a brief description.

These entries create a permanent record that feeds into the general ledger and eventually the trial balance.

The general ledger collects all journal entries organized by account type. It shows the running balance of each account.

Normal Balances and Their Importance

Each account type has a normal balance that indicates whether it typically carries a debit or credit balance. Asset and expense accounts have normal debit balances, so debits increase them and credits decrease them.

Liability, equity, and revenue accounts have normal credit balances, so credits increase them and debits decrease them.

Understanding normal balances helps business owners record transactions correctly. A cash account with a credit balance signals an error because cash should have a debit balance.

These expectations make it easier to spot mistakes during the accounting cycle. The trial balance lists all accounts with their debit or credit balances to verify that total debits equal total credits.

Major Account Types and Their Behaviors

Every account in a business fits into one of five categories. Each category follows different rules for debits and credits.

Assets and expenses increase with debits. Liabilities, equity, and revenue increase with credits.

Assets and Asset Accounts

Asset accounts track what a business owns. This includes cash, inventory, equipment, accounts receivable, vehicles, and property.

When a business gains more of these items, the asset account increases with a debit entry. When it loses them or uses them up, the account decreases with a credit entry.

Cash is the most common asset account. When money enters the business, that’s a debit to cash.

When money goes out, that’s a credit to cash. Accounts receivable tracks money customers owe.

Equipment and inventory also fall under assets.

Debit Effect: Increases the asset

Credit Effect: Decreases the asset

The chart of accounts typically lists asset accounts first. Most businesses group them into current assets like cash and accounts receivable, and long-term assets like buildings and equipment.

Liabilities and Liability Accounts

Liability accounts track what a business owes to others. Common liability accounts include loans payable, accounts payable, credit card balances, and wages payable.

A debit entry decreases a liability account because it means the business paid off some of what it owes. A credit entry increases a liability account because the business took on more debt or obligations.

When a business takes out a loan, it credits the liability account to show the new debt. When it makes a payment on that loan, it debits the liability account to reduce what’s owed.

Debit Effect: Decreases the liability

Credit Effect: Increases the liability

Banks list their deposits as liabilities because they owe that money back to customers. This explains why bank statements show opposite entries from what appears in a business owner’s books.

Equity and Equity Accounts

Equity accounts represent the owner’s stake in the business. This includes the initial investment the owner made, any additional capital contributions, and retained earnings from past profits.

Equity is what’s left after subtracting liabilities from assets. Credits increase equity accounts while debits decrease them.

When an owner invests money in the business, that’s a credit to the equity account. When an owner withdraws money for personal use, that’s a debit to equity.

Retained earnings is an equity account that holds accumulated profits the business hasn’t distributed to owners. At the end of each period, revenue and expense accounts close out into retained earnings.

Debit Effect: Decreases equity

Credit Effect: Increases equity

The equity section on the balance sheet shows how much of the business truly belongs to its owners after all debts are paid.

Revenue and Revenue Accounts

Revenue accounts track income a business earns from its operations. This includes sales revenue, service revenue, interest income, and rental income.

Revenue accounts increase with credit entries and decrease with debits. When a business makes a sale, it credits the revenue account to show the income earned.

Returns or refunds are debited to revenue, reducing the total income.

Revenue appears on the income statement. At the end of each accounting period, revenue accounts close to retained earnings in the equity section.

Debit Effect: Decreases revenue (rare)

Credit Effect: Increases revenue (normal)

The chart of accounts usually lists revenue accounts after all the balance sheet accounts. Different revenue streams often get their own separate accounts for better tracking.

Expense Tracking and Expense Accounts

Expense accounts organize business costs into categories that track spending patterns and support tax deductions. Classifying expenses correctly and managing expense accounts helps business owners maintain accurate records and control cash flow.

Types of Business Expenses

Business expenses fall into two main categories: operating expenses and capital expenses.

Operating expenses cover day-to-day costs like supplies, utilities, and wages. Capital expenses involve long-term assets like equipment and vehicles.

Operating expenses get deducted in the year they occur. For example, a business owner who pays $300 for office supplies records that amount as an expense in the current period.

Capital expenses require a different treatment. Instead of deducting the full cost immediately, businesses spread the expense over several years through depreciation.

A company that buys a $10,000 vehicle might deduct $2,000 per year over five years.

Tax-deductible expenses must meet IRS requirements: they need to be ordinary and necessary for the business. Ordinary means common in the industry, while necessary means helpful for business operations.

Common Expense Accounts

An expense account tracks specific cost categories in the general ledger. Each account receives debits when costs increase and credits when refunds or adjustments occur.

Most small businesses use these standard expense accounts:

- Payroll expenses – wages, salaries, and benefits

- Rent expense – office or retail space payments

- Insurance expenses – business insurance premiums

- Office expenses – supplies and equipment

- Utilities – electricity, water, internet

- Advertising – marketing and promotional costs

- Depreciation – capital asset value reduction

Setting up sub-accounts within main categories improves tracking accuracy. A business might split payroll expenses into separate accounts for salaries, health insurance, and payroll taxes.

Rent, Payroll, and Depreciation

Rent expense is one of the largest fixed costs for businesses with physical locations. When a business pays monthly rent, it debits the rent expense account and credits cash.

A $2,000 rent payment increases the rent expense by $2,000 and decreases cash by the same amount.

Payroll expenses include all costs related to compensating employees. This covers base wages, overtime pay, employer-paid taxes, and benefits like health insurance.

To record payroll, the business makes multiple entries across different expense accounts to capture each component.

Depreciation spreads the cost of long-term assets over their useful life. Unlike rent or payroll, depreciation doesn’t involve actual cash leaving the business.

A company records depreciation by debiting the depreciation expense account and crediting accumulated depreciation.

This method matches the asset’s cost with the revenue it generates over time.

Practical Examples of Debits and Credits in Small Business

Small business transactions follow predictable patterns. These patterns make debits and credits easier to understand once you see them in action.

Sales on credit increase both receivables and revenue. Purchases on credit create both expenses and payables.

Loan transactions affect cash and liability accounts in specific ways.

Making a Sale on Credit

When a business sells goods or services and allows the customer to pay later, two accounts change at once. The business records a debit to Accounts Receivable and a credit to Revenue.

For example, if a landscaping company completes a $2,000 job and invoices the client:

- Debit Accounts Receivable $2,000

- Credit Revenue $2,000

The Accounts Receivable debit increases the asset account because the business now has money owed to it. The Revenue credit increases income because the business earned that money through its work.

When the customer pays the invoice, the transaction shifts from one asset to another. Cash increases and Accounts Receivable decreases:

- Debit Cash $2,000

- Credit Accounts Receivable $2,000

The total assets remain the same, but the business now has usable cash instead of an outstanding invoice.

Purchasing Supplies on Credit

Buying supplies without immediate payment creates a liability called Accounts Payable. The business receives something of value now and agrees to pay later.

If an office buys $500 worth of printer paper and toner on a 30-day payment term:

- Debit Supplies Expense $500

- Credit Accounts Payable $500

The Supplies Expense debit increases the expense account because the business used resources. The Accounts Payable credit increases the liability account because the business owes the supplier money.

When the business pays the bill:

- Debit Accounts Payable $500

- Credit Cash $500

The Accounts Payable debit reduces what the business owes. The Cash credit reduces the asset account as money leaves the bank.

Receiving Loan Proceeds

A business loan increases both assets and liabilities at the same time. The cash account grows because money arrives, and the loan payable account grows because the business takes on debt.

When a small business receives a $25,000 loan:

- Debit Cash $25,000

- Credit Loan Payable $25,000

The Cash debit increases assets because the bank account balance goes up. The Loan Payable credit increases liabilities because the business now owes $25,000 to the lender.

Loan Payment Transactions

Paying back a business loan involves both principal and interest. The principal payment reduces the loan payable, while interest counts as an expense.

For a monthly payment of $600 where $500 goes to principal and $100 is interest:

- Debit Loan Payable $500

- Debit Interest Expense $100

- Credit Cash $600

The Loan Payable debit decreases the liability because the business owes less. The Interest Expense debit increases expenses because interest is a cost of borrowing.

The Cash credit decreases assets as money leaves the account.

Cash Handling and Bank Reconciliation Methods

Cash accounts need regular monitoring to track actual money available versus what the books show. Bank reconciliation ensures every transaction matches between internal records and bank statements.

Cash Accounts and Bank Statements

The cash account in a business’s books tracks all money flowing in and out. This includes physical cash, checking accounts, and savings accounts.

Every debit to cash represents money received, while every credit represents money paid out.

A bank statement shows the same account from the bank’s perspective. The bank records deposits as credits (because it’s a liability they owe to the business) and withdrawals as debits.

This creates a mirror image of the business’s own records.

The ending balance on the bank statement rarely matches the cash account balance on the same date. Outstanding checks haven’t cleared yet.

Deposits in transit haven’t processed. Bank fees and interest may not be recorded in the books yet.

These timing differences are normal and expected.

Tracking Payments and Receipts

Every cash receipt gets debited to the cash account and credited to the source. Customer payments credit Accounts Receivable.

Cash sales credit Sales Revenue. Loan proceeds credit Notes Payable.

Every cash payment gets credited from cash and debited to the destination. Vendor payments debit Accounts Payable.

Supply purchases debit Supplies or Inventory. Loan payments debit Notes Payable and Interest Expense.

The business should record transactions as they occur, not when they clear the bank. A check written on March 28th gets recorded on March 28th, even if it doesn’t clear until April 5th.

This practice matches the accrual basis of accounting and keeps records current.

Reconciling with Your Bank

Bank reconciliation compares the bank statement to the cash account. The process identifies differences and adjusts the books to reflect actual cash position.

Most businesses reconcile monthly. High-volume operations may reconcile weekly.

The process starts with the bank statement ending balance. Add deposits in transit (recorded but not yet on the statement).

Subtract outstanding checks (written but not yet cleared). This produces the adjusted bank balance.

Next, start with the book balance. Add bank credits not yet recorded, such as interest earned or direct deposits.

Subtract bank charges not yet recorded, such as service fees or returned checks. This produces the adjusted book balance.

When both adjusted balances match, the reconciliation is complete.

Any items that adjusted the book balance require journal entries. Bank fees get debited to an expense account and credited to cash.

Interest earned gets debited to cash and credited to interest income.

Modern Bookkeeping Tools and Best Practices

Modern accounting software handles most debit and credit entries automatically. This reduces errors and saves time for small business owners.

The right tools and workflows help maintain accurate records while avoiding common mistakes.

Accounting Software for Small Businesses

Most small businesses use cloud-based accounting software like QuickBooks or Xero to manage their books.

These platforms automatically create journal entries when a business owner records a sale, pays a bill, or receives a payment.

The software posts debits and credits to the correct accounts without requiring manual calculations.

QuickBooks dominates the U.S. market and offers features like automatic bank feeds, invoice tracking, and payroll integration.

Xero provides similar functionality with a different interface that some users find easier to navigate.

Both platforms sync with bank accounts to import transactions automatically.

Some business owners prefer plain-text accounting systems like Beancount, which stores financial data in simple text files.

These tools give complete control over data and work well for people comfortable with command-line interfaces. However, they require more technical knowledge than mainstream options.

The key advantage of any modern accounting software is automation. Instead of manually recording each debit and credit, the software handles the technical work behind the scenes.

Business owners can focus on entering transaction details while the system maintains balanced books.

Automating Journals and Financial Reporting

Modern bookkeeping software creates journal entries automatically for routine transactions. When a business records an invoice, the system debits accounts receivable and credits revenue.

Payment processing tools like QuickBooks Payments post entries directly to the books when customers pay.

Automation reduces the need for manual journal entries to specific situations. Business owners typically only create manual entries for depreciation, accruals, corrections, or owner contributions and withdrawals.

Most accounting software flags unbalanced entries before saving them, catching errors immediately.

Real-time financial reporting gives business owners instant access to profit and loss statements, balance sheets, and cash flow reports.

The system updates these reports as transactions occur, eliminating the need to wait for month-end closing.

Many platforms also generate reports needed for tax filing and loan applications.

Bank reconciliation features compare imported bank transactions against recorded entries. The software highlights discrepancies so bookkeepers can identify missing transactions or data entry errors.

This regular checking keeps the books accurate throughout the year.

Avoiding Common Debit and Credit Mistakes

Mixing personal and business transactions creates serious problems in bookkeeping records. Business owners should maintain separate bank accounts and credit cards for company expenses.

When personal funds mix with business transactions, tracking true profitability becomes difficult and tax complications arise.

Incorrect account classification leads to misleading financial reports. Recording a loan payment as an expense instead of splitting it between interest expense and loan principal reduction distorts both the income statement and balance sheet.

Understanding which account type to use prevents these errors.

Many business owners forget to record all transactions, especially small cash purchases or owner withdrawals. Every dollar that enters or leaves the business needs a corresponding entry.

Incomplete records make financial statements unreliable and create problems during tax season.

Modern accounting software prevents most technical errors by automating debit and credit logic. Business owners still need to verify that transactions post to the correct accounts.

Regular review of financial statements helps catch classification errors before they compound. Working with a bookkeeper or accountant provides additional oversight for complex transactions like depreciation or accruals.

Frequently Asked Questions

Debits increase assets and expenses while credits increase liabilities, equity, and revenue. Every transaction in double-entry bookkeeping requires equal debit and credit entries to keep financial records balanced.

What is the difference between a debit and a credit in accounting?

A debit is an entry on the left side of an account that increases assets and expenses. A credit is an entry on the right side that increases liabilities, equity, and revenue.

The key difference lies in how they affect different account types. When a business records a debit to an asset account like cash, that account increases.

When it records a credit to the same cash account, that account decreases.

For liability accounts, the opposite is true. A credit increases what the business owes, while a debit reduces those obligations.

This opposite behavior confuses many business owners at first. The system works because it tracks both sides of every transaction, showing where money comes from and where it goes.

How do debits and credits work in a journal entry?

Every journal entry must include at least one debit and one credit. The total dollar amount of debits must equal the total dollar amount of credits.

When a business makes a sale, it debits accounts receivable and credits sales revenue for the same amount. This shows both the money owed to the business and the income earned.

When paying bills, the business debits an expense account and credits cash. The debit records the cost incurred while the credit shows the money leaving the bank account.

A single transaction can affect more than two accounts. The business must still ensure that total debits match total credits across all affected accounts.

Can you provide common debit and credit examples for small business transactions?

Purchasing inventory with cash requires debiting the inventory account and crediting the cash account. Both accounts are assets, but inventory increases while cash decreases.

Recording a customer sale on credit means debiting accounts receivable and crediting sales revenue. This captures both the money owed and the income earned.

Paying employee wages involves debiting wage expense and crediting cash. The expense account increases to reflect the cost while cash decreases to show the payment.

Taking out a business loan requires debiting cash and crediting notes payable. Cash increases from receiving the funds while liabilities increase to reflect the debt owed.

Paying off accounts payable requires debiting the accounts payable account and crediting cash. This reduces both the liability owed and the cash on hand.

How do debits and credits affect the balance sheet and income statement?

The balance sheet shows assets, liabilities, and equity at a specific point in time.

Debits increase asset accounts on the balance sheet. Credits increase liability and equity accounts.

When a business debits cash, the asset amount grows on the balance sheet.

When the business credits accounts payable, the liability increases on the balance sheet.

The income statement tracks revenue and expenses over a period of time.

Credits increase revenue accounts on the income statement. Debits increase expense accounts on the income statement.

Recording a sale by crediting revenue adds that income to the income statement.

Debiting an expense account adds that cost to the income statement.

What are the basic rules for when to debit or credit each account type?

Asset accounts increase with debits and decrease with credits.

This includes cash, inventory, equipment, and accounts receivable.

Expense accounts increase with debits and decrease with credits.

Liability accounts increase with credits and decrease with debits.

This applies to accounts payable, loans, and credit card balances.

Equity accounts increase with credits and decrease with debits.

This includes owner’s equity, retained earnings, and common stock.

Revenue accounts increase with credits and decrease with debits.

All income the business earns gets recorded as a credit to revenue.

A simple memory tool groups these accounts by behavior.

Expenses and assets increase with debits. Liabilities, equity, and revenue increase with credits.

How do you balance debits and credits when entering a journal entry in QuickBooks?

QuickBooks uses double-entry bookkeeping. The software requires you to make balanced entries.

For many common transactions, QuickBooks automatically creates the debit and credit sides. When you record a bank deposit, QuickBooks debits the bank account.

The software prompts you to select which revenue or other account to credit. Both sides must equal the same amount.

For bill payments, the system debits accounts payable and credits the bank account. You simply select the bill to pay and the amount.

Manual journal entries give you full control over both sides. QuickBooks displays a running total of debits and credits as you make entries.

You cannot save the entry until debits equal credits. If the totals do not match, QuickBooks shows the difference.

You must add or adjust entries until both sides balance. The software also flags entries with unusual account combinations.

This helps you catch errors before they affect financial reports.

Leave a Reply